The gas turbine industry just hit a wall it didn’t see coming.

After years of declining orders and market uncertainty, demand exploded. AI data centers need power yesterday. Coal plants are shutting down faster than anyone planned. The grid can’t keep up.

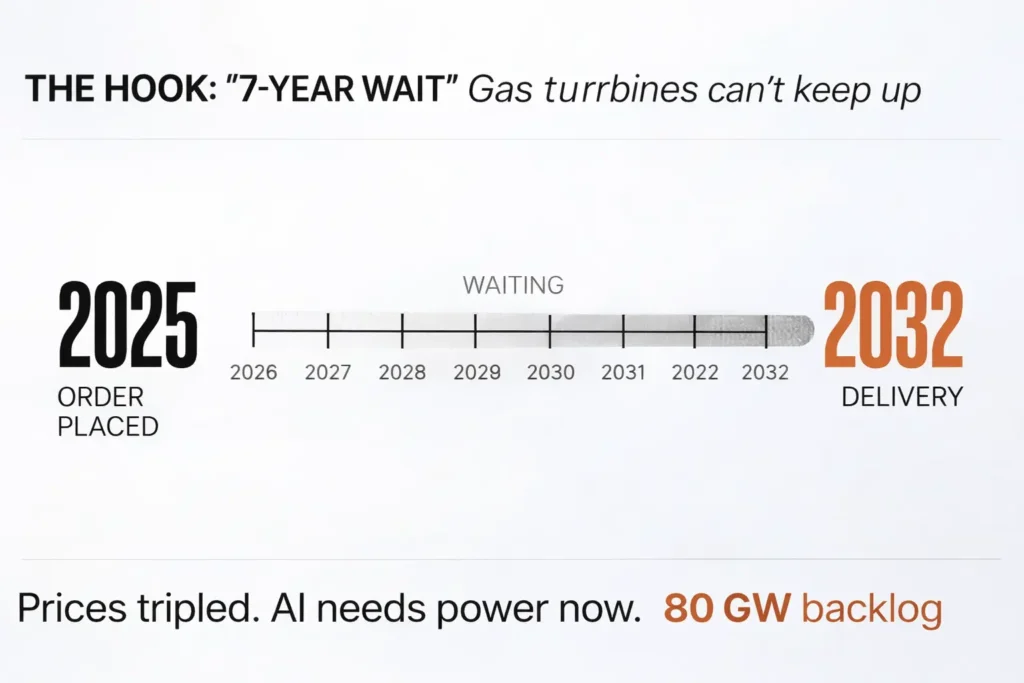

Now manufacturers face backlogs stretching to 2029 and beyond. Prices have tripled in 24 months. Wait times range from one to seven years depending on the model.

This isn’t a temporary supply hiccup. It’s a structural mismatch between what the market needs and what the industry can deliver. And the next ten years will determine whether gas turbines remain the backbone of dispatchable power or get displaced by technologies that can scale faster.

The Demand Drivers Reshaping the Market

Two forces are colliding to create unprecedented turbine demand.

First, AI data centers are consuming electricity at rates that make traditional grid connections impossible. These facilities need massive loads delivered now, not in five years when the utility finishes upgrading transmission lines. Grid connection delays push operators toward on site generation.

Aeroderivative turbines solve this problem. They install quickly, scale modularly, and start fast enough to serve as both primary generation and backup to intermittent renewables.

GE Vernova’s CEO expects gas turbine reservations to sell out through 2030 by the end of 2026. The company ended 2025 with an 80-GW backlog stretching into 2029. They booked 18 GW of orders in Q4 2025 alone.

Second, coal retirements are accelerating globally. Asia Pacific markets are transitioning aging plants to combined cycle gas turbines valued for efficiency and lower emissions. This isn’t a short term trend. It’s a multi decade infrastructure replacement cycle.

General electricity demand is rising sharply in developing regions where GE Vernova and Mitsubishi have historically dominated. These aren’t speculative projects. They’re essential infrastructure replacing end-of-life assets.

The Bottleneck Nobody Planned For

Manufacturing gas turbines requires specialized materials and skilled labor that can’t scale overnight.

EPRI experts report that rotor forgings and hot-section blades have emerged as primary bottlenecks. Some large frame turbines are shipping without rotors or blades. Installation happens later onsite just to maintain construction schedules.

That’s not a workaround. That’s desperation.

Wait times for gas fired turbines now range from one to seven years depending on the model. As of February 2025, OEMs are quoting upwards of five to seven years for new orders. Competition is fierce. Those who wait longer to place orders will wait even longer to receive equipment.

The price impact is brutal. Gas turbines have increased threefold in just 24 months, according to NextEra CEO John Ketchum. Duke Indiana’s latest procurement for the Cayuga combined cycle plant reached $2,340 per kilowatt, 36% higher than expected in the prior year’s resource plan. That translates to a $900 million cost overrun for a 1,476 MW plant.

You can’t budget around that kind of volatility.

Why Manufacturers Aren’t Racing to Expand Capacity

The gas turbine industry has seen this movie before. Boom periods followed by devastating busts. Manufacturers who overinvested in capacity during the shale gas boom got burned when orders collapsed.

Industrial gas turbine OEMs share many of the same supply chain core component suppliers as the booming aerospace industry. This creates direct competition for critical materials and manufacturing capacity between aviation and power generation sectors.

GE Vernova is investing $600 million to expand U.S. capacity. They plan to deliver up to 80 heavy duty gas turbines per year, adding 20 GW annually. But the company’s CEO stated they don’t yet see justification for capacity increases beyond the previously announced 20 GW/year goal by Q3 2026.

This is notable. GE Vernova has $16 billion in cash available for deployment by 2028. They’re choosing not to deploy it aggressively into manufacturing expansion despite record backlogs.

The market is dominated by three major players. GE Vernova commands 36.515% market share, Siemens Energy holds 27.795%, and Mitsubishi Power controls 19.004%. This concentration means limited competitive pressure to rapidly expand capacity. The top players can manage backlogs without fear of losing market position to nimble competitors.

Forecast data shows unit production fluctuating between 489 and 551 units annually from 2025 to 2034. No dramatic expansion trajectory despite rising demand.

The Grid Reliability Crisis Hiding in Plain Sight

Multi-year delays in turbine delivery pose a systemic risk to grid reliability.

Coal retirements are accelerating. Renewable penetration is increasing. If utilities can’t bring dispatchable power capacity online in time, grid stability will suffer during periods of high demand or low renewable output.

By the end of 2024, utilities’ planned gas turbine deployments through 2030 had doubled from just under 25 GW to over 45 GW. This analysis covered 104 utilities representing just over half of U.S. electricity demand.

Meanwhile, Mitsubishi states that turbines ordered today won’t deliver until 2028 to 2030.

The math doesn’t work. Utilities are planning for capacity they can’t secure in time to meet their own timelines.

Engie pulled out of two gas plant projects in Texas late in 2024 due to delivery backlogs stretching past 2029. This isn’t hypothetical. Projects are already being canceled because equipment simply isn’t available.

Emergency measures could follow. Delayed coal plant retirements. Increased reliance on older, less efficient peaking plants. Both outcomes undermine emissions reduction goals and increase costs.

The Technology Competition Window Opening

Battery storage systems are scaling rapidly with improving economics. They’re not yet competitive for long-duration backup power, but the gap is closing.

If turbine delivery delays extend beyond 2029 to 2030, battery technology may advance sufficiently to capture market share that would otherwise go to gas turbines. The industry’s hesitation to invest in capacity expansion could become a self fulfilling prophecy.

Data center operators facing multi year grid connection delays are already deploying creative workarounds. They’re using aeroderivative gas turbines based on retired commercial aircraft engines. GE CF6 80C2 engines from 767s can deliver 48 megawatts each and be operational in under 6 months, compared to 18 to 24 month lead times for new manufacturing.

Approximately 1,000 of these aircraft engines are expected to retire over the next decade. That’s a stopgap solution, but it demonstrates the pressure building in the market.

When your customers start buying used airplane engines to generate electricity, you have a supply problem.

The Hydrogen Pathway and Long-Term Viability

Gas turbines are positioning themselves as increasingly green energy sources through higher hydrogen concentrations in fuel mixtures.

The industry’s ultimate goal is 100% green hydrogen operation, which would dramatically reduce environmental impact. This transition pathway represents a critical differentiator for turbines in the long term energy landscape.

But infrastructure barriers remain significant. Hydrogen supply networks, pipeline systems, and storage facilities are underdeveloped. The technology exists. The infrastructure doesn’t.

This creates an interesting dynamic. If gas turbines can successfully transition to hydrogen, they extend their viability well beyond current projections as the world decarbonizes. If they can’t, battery storage and other technologies will gradually erode their market position.

The next ten years will determine which scenario plays out.

What This Means for Different Stakeholders

For utility operators and project developers, early procurement is now mandatory, not optional. The days of ordering turbines with 12 to 18 month delivery windows have ended. Multi year planning horizons are the new normal.

You need to place orders years in advance simply to secure equipment. This fundamentally changes how you plan capital projects and manage risk.

For manufacturers, the data suggests that capacity expansion investments, while risky given historical boom bust cycles, may be justified by structural demand drivers that differ from previous periods. AI data centers, coal retirements, and renewable integration represent sustained trends, not temporary spikes.

The question is whether manufacturers will recognize this difference in time to capture the opportunity.

For policymakers, supply constraints highlight the need for coordinated planning that accounts for long lead times in dispatchable power infrastructure. Regulatory changes to accelerate permitting and interconnection processes may be necessary to prevent grid reliability crises.

You can’t wish away seven year lead times with policy. But you can create frameworks that help utilities plan around them.

The Forecast That Matters Most

Market forecasts indicate steady growth in installed capacity across all power classes from 2025 to 2034. The 250 to 500 MW and 500 to 750 MW classes represent the largest segments, reflecting their role in utility scale power generation and combined cycle plants.

Smaller capacity classes maintain consistent but minor market share, suggesting limited growth in distributed generation applications despite potential for modular deployment.

Siemens Energy reports a record order backlog of €133 billion (US$148 billion), with 65% of gas turbine orders in fiscal year to date coming from data centers. CEO Christian Bruch stated that “for the first time, I see that across all frame sizes there has been super high demand.”

The demand is real. The orders are real. The question is whether supply can catch up before alternatives become more attractive.

The Reality Check

While manufacturers are expanding facilities to increase gas turbine production, changes in production output will not happen overnight. Orders are robust and the market sits on solid footing, but production increases remain tempered by structural challenges.

This creates a fundamental disconnect. Strong demand signals long-term market health, but supply constraints limit the industry’s ability to capitalize on the opportunity.

The concentration of manufacturing capacity among a few Western and Japanese firms, combined with extended backlogs, creates energy security vulnerabilities for developing nations seeking to expand power generation. Countries unable to secure turbine orders early may face prolonged electricity shortages.

This could accelerate efforts by nations like China and India to develop domestic turbine manufacturing capabilities, reshaping the competitive landscape over the next decade.

The gas turbine industry faces a paradox. Demand has never been stronger. The long-term outlook appears solid. But the inability to scale supply quickly enough may open doors for competing technologies or new market entrants.

The next ten years will test every assumption about how power infrastructure gets built, who builds it, and how fast the market can adapt when the old playbook stops working.

You’re watching an industry at an inflection point. What happens next depends on whether manufacturers bet big on sustained demand or play it safe and risk losing market position to technologies that can move faster.

Either way, the decisions made in the next 24 months will shape the power generation landscape for the next quarter century.